SNR Tax Care — Accounting Desk Notes

Balance Sheet Finalization: 8 Proven Steps to Error‑Free Accounts

A complete, no-jargon walkthrough of Balance Sheet Finalization — the process every business uses to close its books, catch errors, and file accurate accounts at year end.

Updated 2024

9 min read

By SNR Tax Care Team

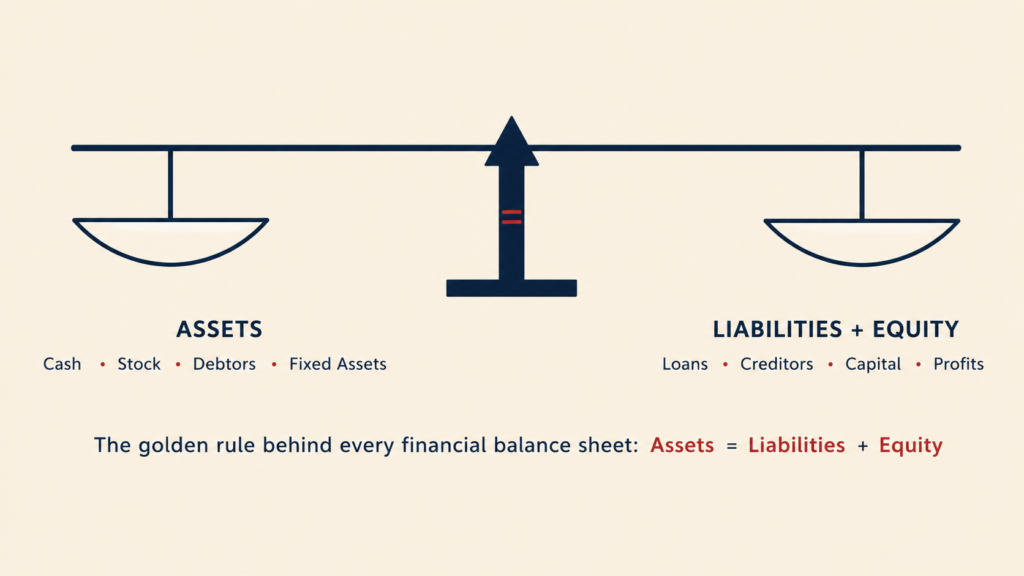

A Balance Sheet is a financial statement that shows where a company stands on a specific date — what it owns, what it owes, and what belongs to its owners. Balance Sheet Finalization is the disciplined, step-by-step process of checking, adjusting, and approving that statement so it's accurate, compliant, and ready to be filed.

Skip a step and the numbers look fine on the surface but quietly mislead everyone who relies on them — owners, lenders, and tax authorities alike. Below is the exact 8-step sequence our team at SNR Tax Care follows for every client, with real worked examples at each stage.

On this page

Step 1 — Extract the Trial Balance

Step 2 — Pass Adjustment Entries

Step 3 — Bank Reconciliation (BRS)

Step 4 — Ledger Scrutiny

Step 5 — Prepare the P&L Account

Step 6 — Draft the Balance Sheet

Step 7 — Review & Internal Verification

Step 8 — Final Sign-Off & Filing

STEP 01 / 08

Extract the Trial Balance

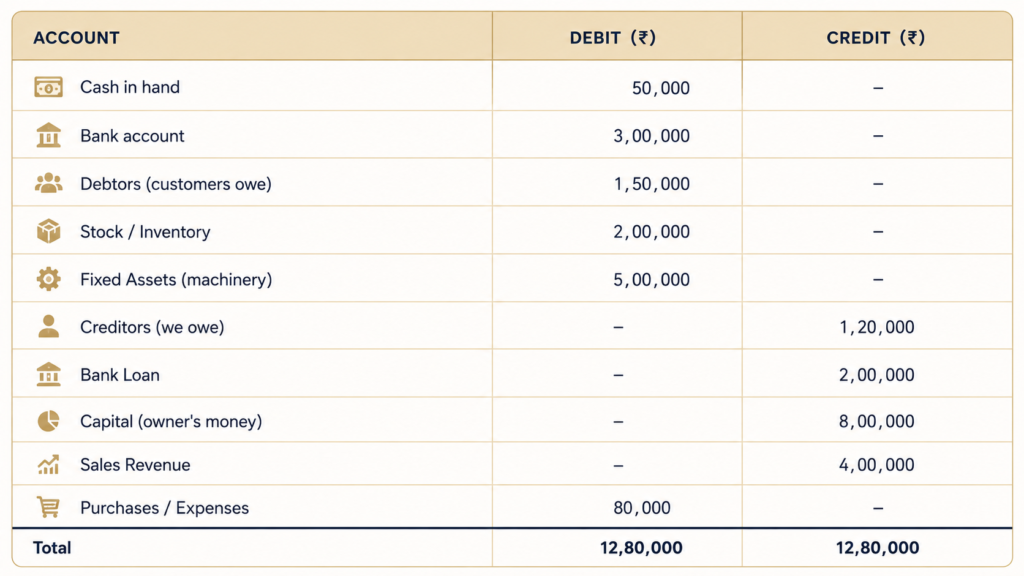

Every round of Balance Sheet Finalization starts with the Trial Balance — a list of every ledger account's closing balance, arranged in two columns: Debit and Credit. If both columns don't match, there's a bookkeeping error to fix before anything else happens.

Sample Trial Balance as on 31st March 2024 — the starting point of Balance Sheet Finalization.

STEP 02 / 08

Pass Adjustment Entries

Before the books can close, anything missed during the year needs to be recorded. These are the adjustment entries, and missing even one quietly distorts every figure that follows.

Depreciation — reduction in asset value over time

Outstanding expenses — bills received, not yet paid

Prepaid expenses — payments made in advance

Accrued income — earned, not yet received

Example: Machinery worth ₹5,00,000 depreciates at 10% a year. Entry: Depreciation A/c Dr ₹50,000 → To Machinery A/c ₹50,000. Machinery now shows ₹4,50,000 on the Balance Sheet.

STEP 03 / 08

Bank Reconciliation Statement (BRS)

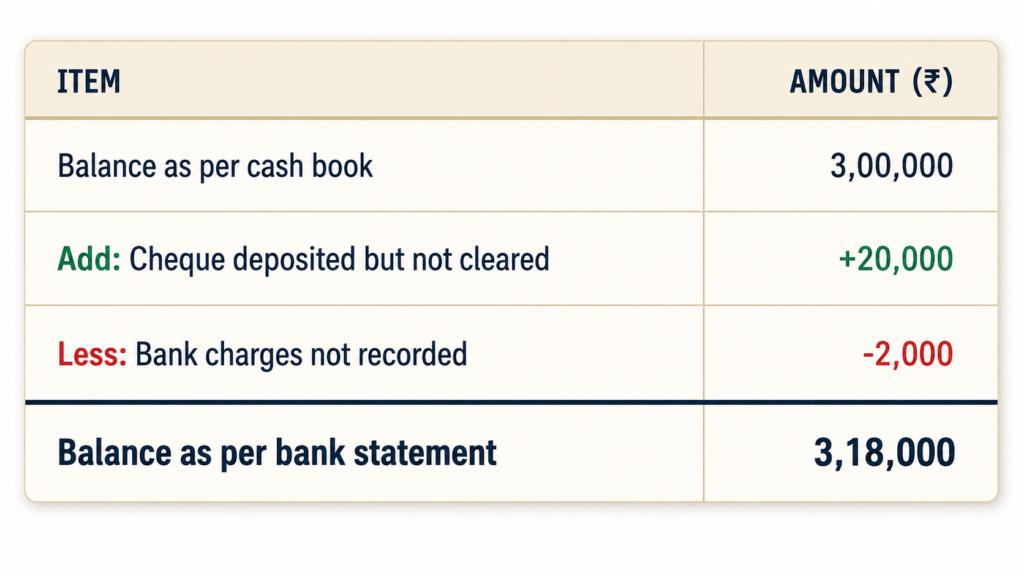

The Bank Reconciliation Statement compares the company's internal cash book against the actual bank statement, surfacing differences such as cheques issued but not yet cleared, or bank charges not yet recorded.

BRS confirms the difference between books and bank is fully explained.

STEP 04 / 08

Ledger Scrutiny

Next, every major ledger account is examined one by one for correctness — this is ledger scrutiny, and it's where most genuine errors are caught.

1. Debtors — are outstanding amounts genuine and collectible?

2. Creditors — do balances match supplier invoices?

3. Fixed assets — are additions and disposals recorded correctly?

4. Loans — is principal and interest calculated correctly?

5. Stock — does physical stock match the book figure?

Example: Debtors show ₹1,50,000 outstanding. Scrutiny reveals one customer owing ₹20,000 hasn't paid in two years, so a provision for bad debts of ₹20,000 is created — net debtors drop to ₹1,30,000.

STEP 05 / 08

Prepare the Profit & Loss Account

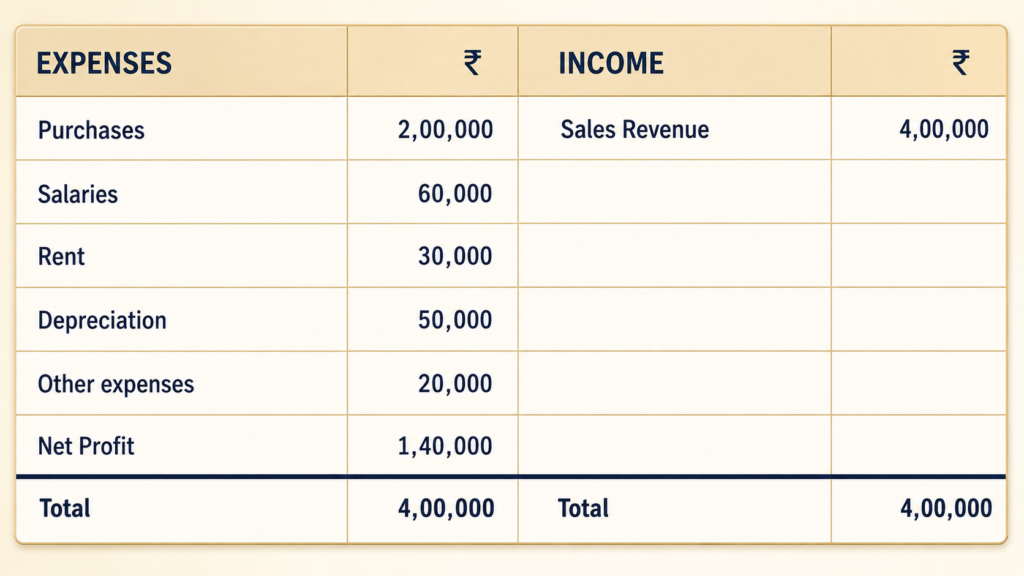

The Profit & Loss Account totals every income and expense for the year into a single Net Profit or Net Loss figure, which then flows straight into the equity side of the Balance Sheet.

STEP 06 / 08

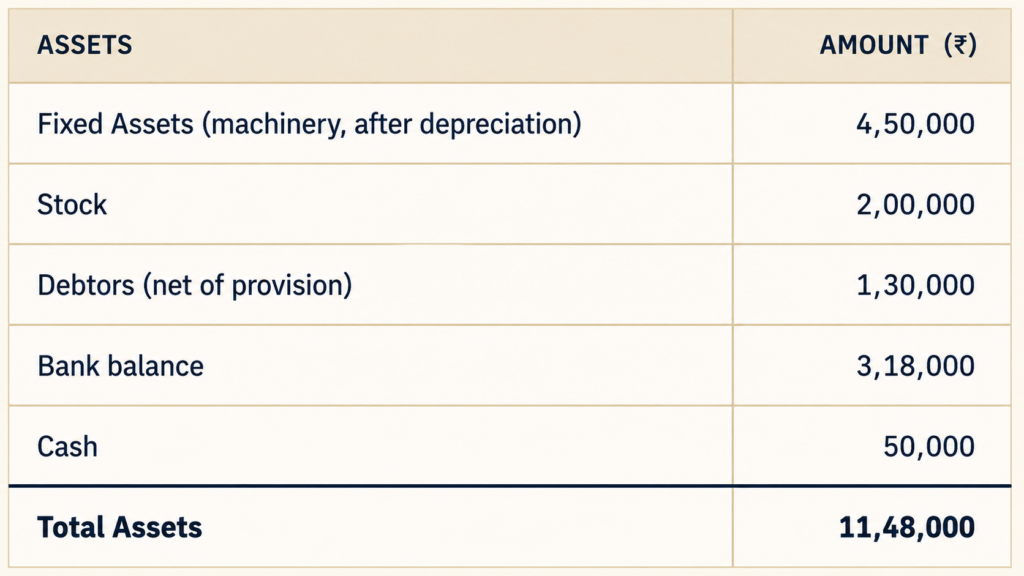

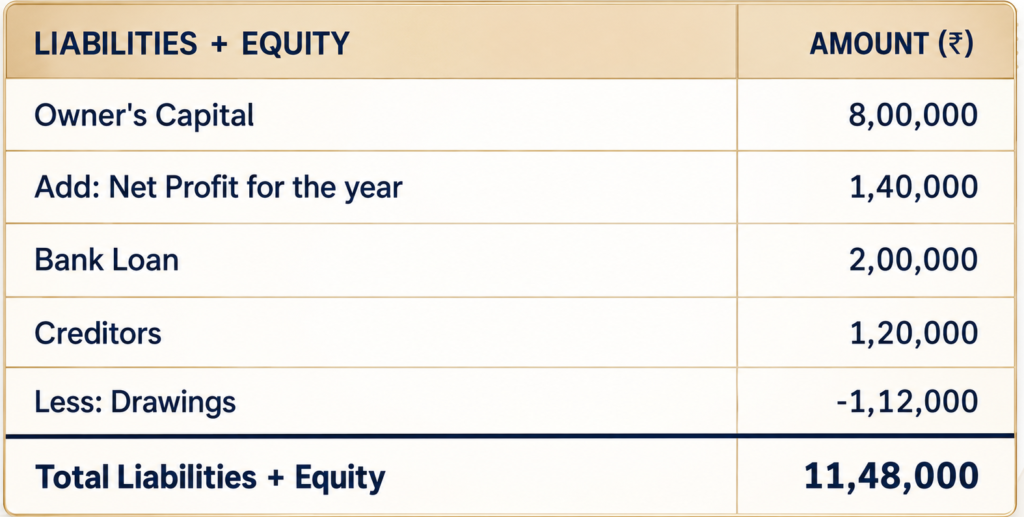

Draft the Balance Sheet

With every adjustment made and the Profit & Loss figure ready, the Balance Sheet itself can finally be drafted — assets on one side, liabilities and equity on the other.

Both sides total ₹11,48,000 — the Balance Sheet balances.

STEP 07 / 08

Review and Internal Verification

Before anyone signs anything, a senior accountant, CFO, or internal auditor reviews the draft — confirming it tallies, that disclosures like contingent liabilities are included, and that keyratios look reasonable.

Example check: Current Ratio = Current Assets ÷ Current Liabilities = (2,00,000 + 1,30,000 + 3,18,000 + 50,000) ÷ 1,20,000 = 5.8 — a healthy figure, meaning the company can comfortably cover its short-term dues.

STEP 08 / 08

Final Sign-Off and Filing

Once reviewed and approved, the Balance Sheet is signed by the authorized person — Director, Partner, or Proprietor — and by the auditor where required, then filed with the relevant authority.

Example: ABC Pvt Ltd's Board meets on 30th April 2024, approves the Balance Sheet for the year ended 31st March 2024, the auditor signs the report, and it's filed with the ROC before the due date.

Related reading on SNR Tax Care

Key Points to Remember

. The Balance Sheet always balances: Assets = Liabilities + Equity.

. Finalization happens at the end of every accounting period — monthly, quarterly, or yearly.

. Adjustment entries are critical — missing them produces wrong figures downstream.

. Bank reconciliation keeps the cash position accurate and explainable.

. Net Profit from the P&L Account always flows into the equity side.

. Always get the final draft reviewed and signed before filing.

Need help with Balance Sheet Finalization?

SNR Tax Care handles trial balances, reconciliations, and year-end filing for businesses across India — so your books close right, the first time.