7 Essential Bookkeeping & Accounts

Maintenance

Tips Every Business Must Know

- By SNR TaxCare Experts

- Updated: June 2024

- 12 min read

- Bookkeeping Guide

compliant, profitable, and financially healthy. This guide by SNR TaxCare covers everything from the golden rules to practical examples — so you can manage your accounts with confidence.

📋 Table of Contents

2. Basic Concepts: Assets, Liabilities & Capital

3. Single Entry vs Double Entry Bookkeeping

4. The 3 Golden Rules of Debit & Credit

5. Books of Accounts You Must Maintain

6. Journal Entries & Ledger Posting

7. Trial Balance & Final Accounts

8. Day-to-Day Accounts Maintenance Practices

9. Common Bookkeeping Mistakes to Avoid

10. Quick Reference: What Goes Where?

What is Bookkeeping?

Bookkeeping: Recording Every Business Transaction

Accounts ledger • Journal entries • Financial records

Basic Concepts in Bookkeeping

fundamental concepts:

🏗️

Assets

Things your business owns — cash,

equipment, vehicles, buildings, stock.

💳

Liabilities

Things your business owes — loans, unpaid bills, credit from suppliers.

👤

Capital / Equity

The owner's investment in the business. What remains after paying liabilities.

💰

Income / Revenue

Money earned from selling goods or services to customers.

📉

Expenses

Money spent to run your business — rent, salary, electricity, etc.

The Golden Accounting Equation

Assets = Liabilities + Capital

Single Entry vs Double Entry Bookkeeping

1. Single Entry System

2. Double Entry System ✅ Recommended

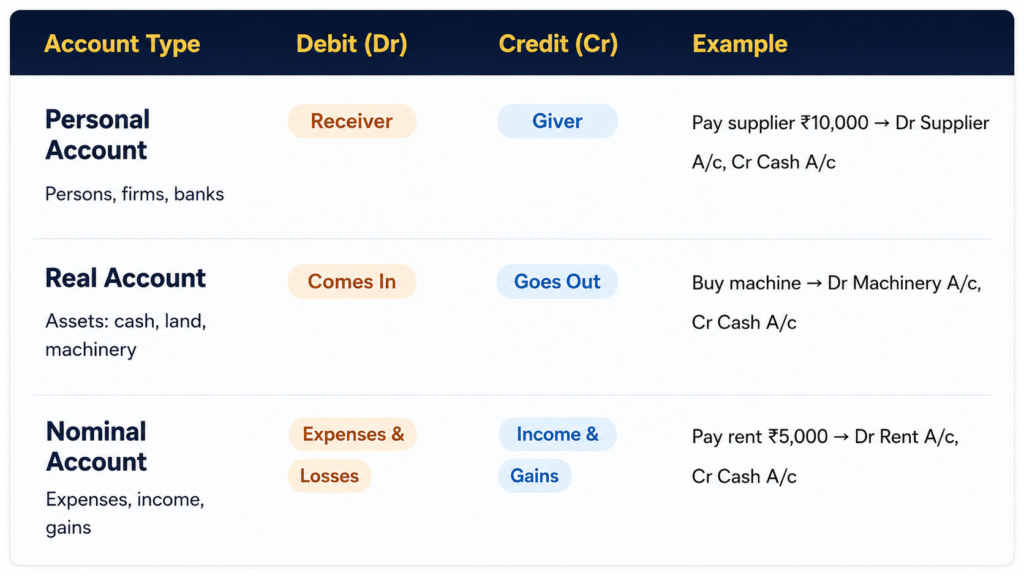

The 3 Golden Rules of Bookkeeping — Debit & Credit

3 Golden Rules of Debit & Credit

Personal • Real • Nominal Accounts

Books of Accounts You Must Maintain

Journal (Day Book)

Ledger

Cash Book

Purchase Book

Sales Book

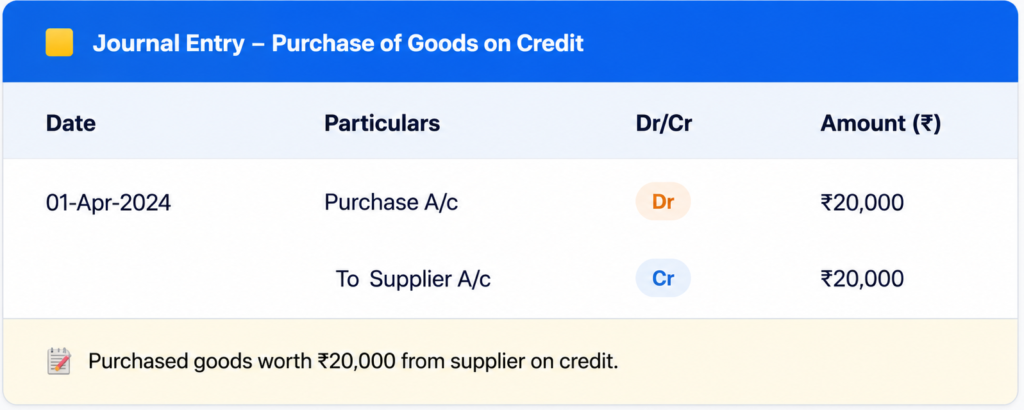

Journal Entries & Ledger Posting — Practical Examples

Step 1: Create a Journal Entry

Step 2: Post to the Ledger

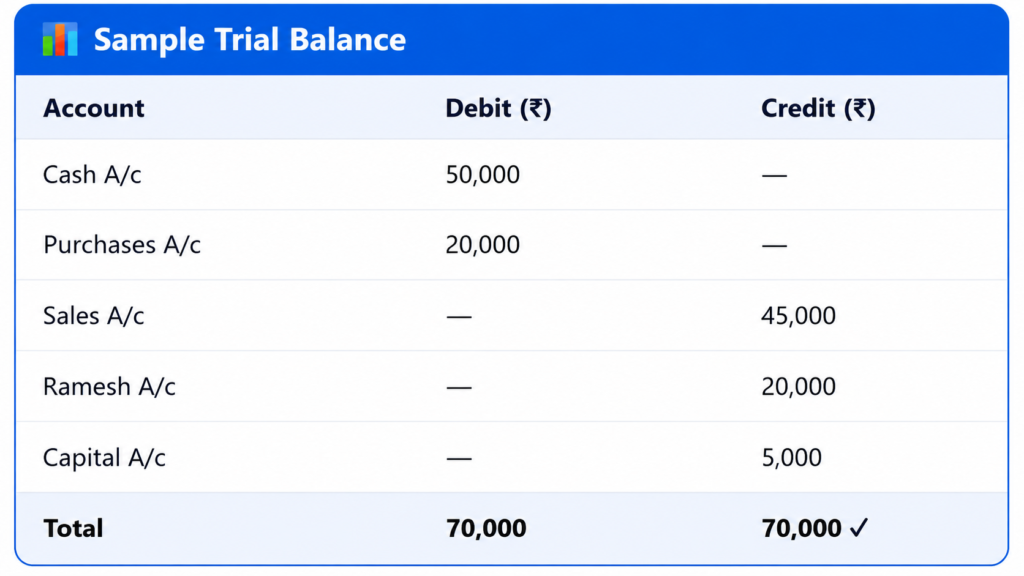

Trial Balance & Final Accounts

Final Accounts — Three Key Statements

📈

Trading Account

Shows Gross Profit = Sales minus Cost of Goods Sold.

💹

Profit & Loss Account

Shows Net Profit = Gross Profit minus all operating expenses.

🏦

Balance Sheet

Snapshot of the business showing all Assets = Liabilities + Capital on a specific date.

Day-to-Day Accounts Maintenance Best Practices

Daily Accounts Maintenance — Best Practices

Record daily • Reconcile bank • Track GST • Audit-ready books

1. Record Transactions Daily

Enter every transaction on the same day it happens. Never leave bookkeeping entries for later — this is the #1 rule for clean accounts.

2. Keep All Source Documents

Always attach bills, invoices, receipts, and bank slips to your records. These are required for GST audits and income tax assessments.

3. Monthly Bank Reconciliation

Compare your Cash Book with your bank statement every month. This process — called Bank Reconciliation — catches errors and prevents fraud.

4. Track Debtors & Creditors

Maintain a separate ledger for each debtor (who owes you) and creditor (who you owe). Know exactly how much is outstanding at all times.

5. File GST Records Accurately

In India, every transaction must include GST Input Tax Credit (ITC) and Output Tax. Accurate bookkeeping makes your GSTR-1 and GSTR-3B filing effortless.

Common Bookkeeping Mistakes to Avoid

correct them early:

Always double-check your daily entries.

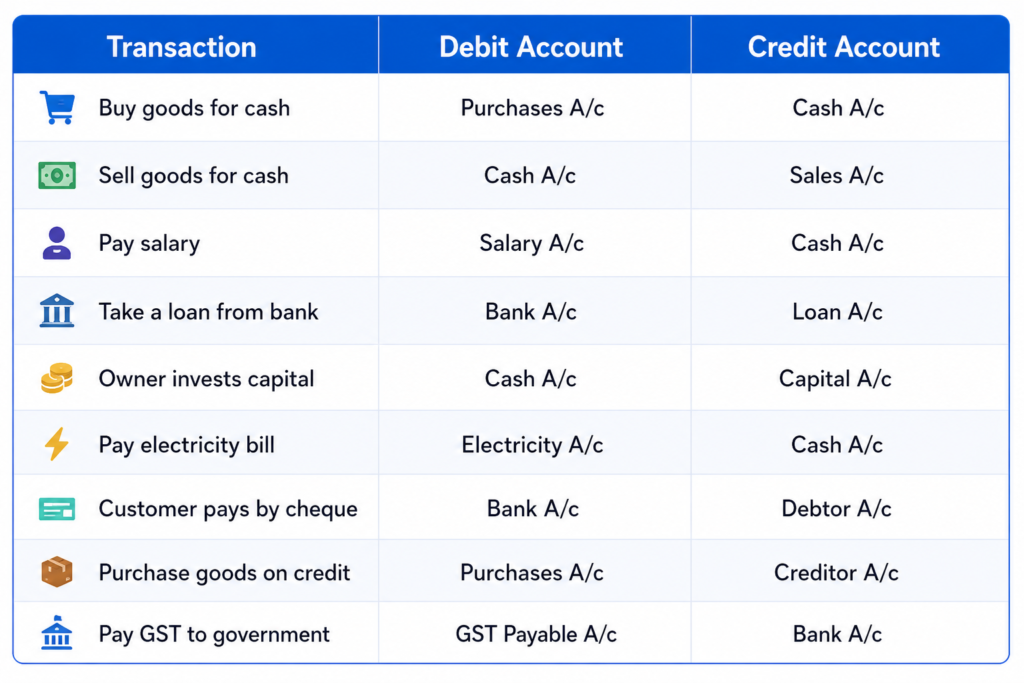

Quick Reference: What Goes Where?